Responsive Benefits of Entry

Granular forward trade incentivizes a more responsive grid

The U.S. electricity grid faces unprecedented load growth. Earlier this year, Texas grid operator ERCOT forecast new data centers would add 77 GW of load to the grid between 2025 and 2030, driving a 121% increase in total load. Even the expectation has increased 64% over the prior year. Now, this is not set in stone - the signals are speculative, and changes in market conditions or oversaturation may drive these numbers up or down. The grid thus requires not only more significant generation and grid infrastructure, but especially the market signals to drive the right investment. Forward trade of energy and options can provide the signals needed to direct investment quickly in response to changes in market conditions.

In this post, we show how the forward market provides reactive price signals. We use our proprietary ERCOT backcast to simulate a demand shock in a market with granular energy forwards and options, and derive Benefit of Entry calculations (implied profits) for generators from the forward and option prices. The analysis shows how the forward market immediately translates participants' changing beliefs into price signals. When market load expectations shift, prices and entry incentives react immediately rather than waiting for the next capacity auction or end-of-year analysis. The result is a live look at incentives for generation entry and exit, facilitating faster investment in the best new supply to meet changes in load.

Demand Shock: New Datacenter Load

We simulate a shock in expected demand — 2 GW or 4 GW — resulting from the newly announced data centers. Higher prices in the forward market follow, reflecting participants’ beliefs that pricing in the spot and day-ahead markets will be higher. In turn, higher pricing motivates new generation.

Model

We simulate this increase in expected demand using a model of an energy-only grid with a single system-wide hourly day-ahead price. We simulate day-ahead pricing using a merit-order model. Forwards and options of the spot price are traded at the same hourly granularity up to four years in advance of the spot. See our working paper for more details on the model.

Incentives for entry are calculated by comparing two quantities: the average cost of entry, as provided by EIA data, and the benefit of entry, which is the value of the expected future cash flows from the generation. Those cash flows can come from either selling forwards or options. At a simple level, if the value of the future expected cash flows exceeds the cost of entry, building the generation is profitable.

Forward Pricing

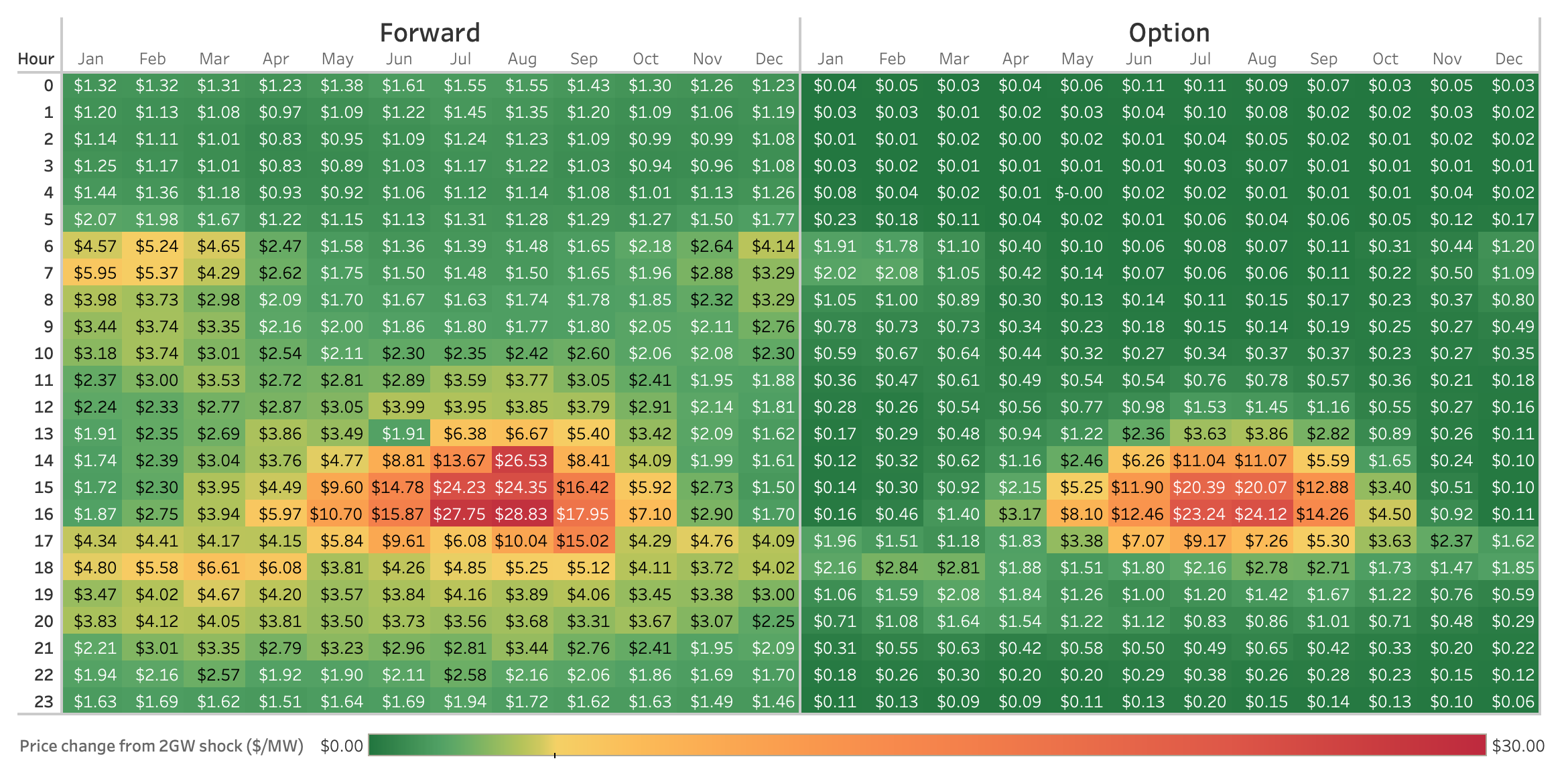

Prices increase following the shift in beliefs and increased demand hedging. Figure 1 shows the magnitude of the jump by hour of the day and month of the year, for forwards and $200 call options, respectively. The largest changes occur during the tightest hours for the Texas grid, summer afternoons.

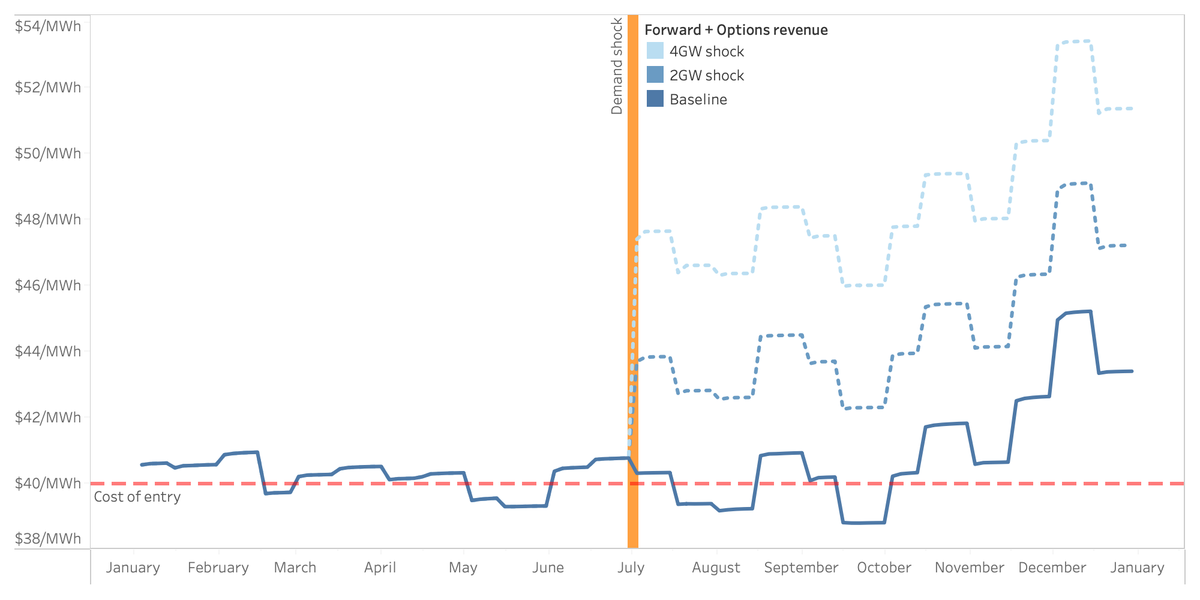

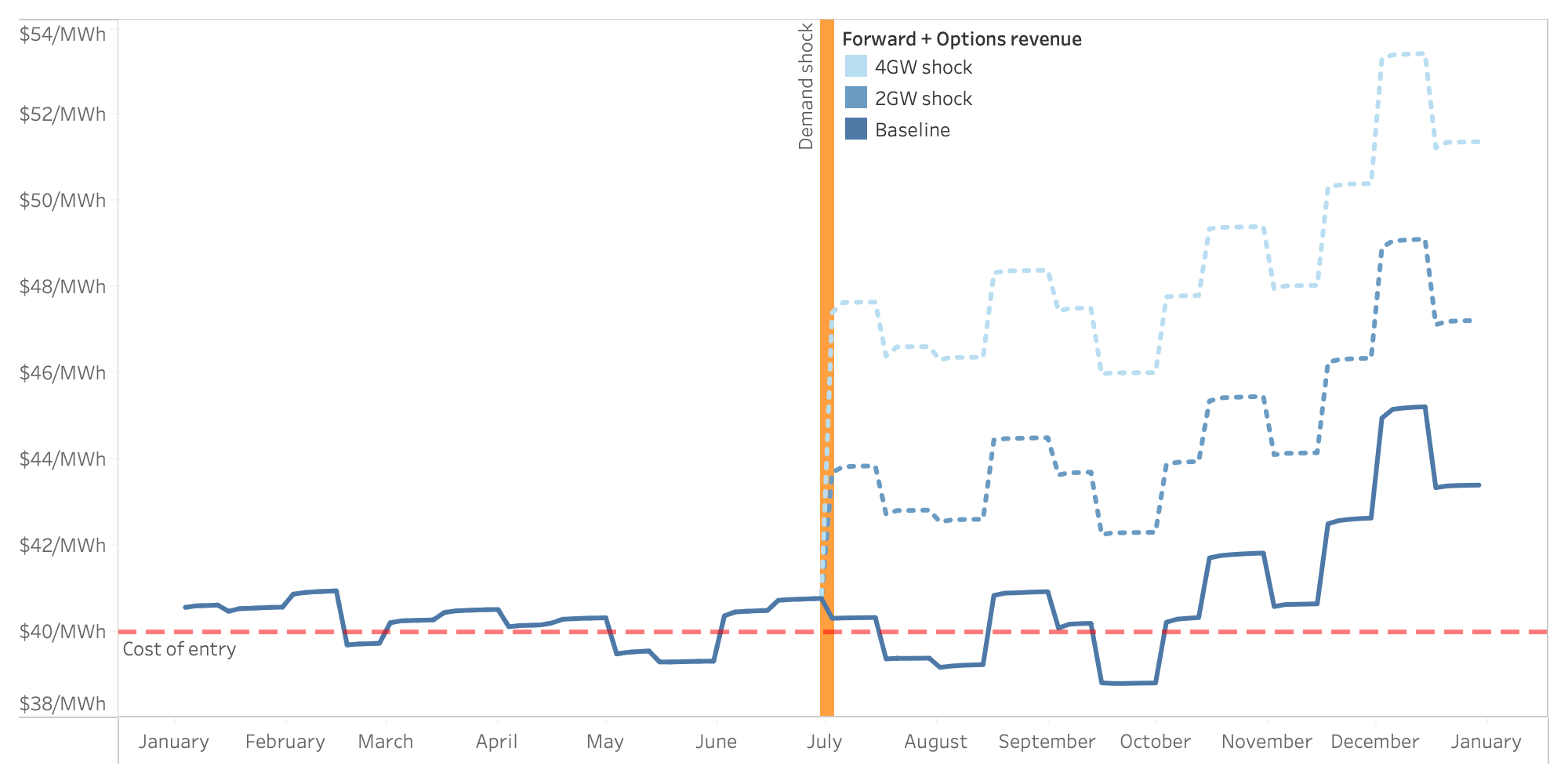

Entry Incentives

Entry of new generation is incentivized when the value of expected cash flows exceeds the cost of building the generation. In Figure 2 below, we show how aggregate incentives react: the increase in prices pushes the benefits from marginal to significantly profitable, immediately incentivizing new development.

With granular trade of forward energy and options, expected cash flows for both base load and peak loads can be directly read from the pricing of the forwards and options. Expected probabilities of option exercise are implied from pricing. Using these quantities for all time periods across a calendar year, we let participants calculate a hedged strategy for a generator as follows:

Maximize annual hedged forward and option profits

subject to:

1. options + forwards quantity at operational capacity

2. total annual utilization matches EIA data

We adopt the same utilization as the EIA data underlying the Cost of Entry numbers, allowing for a direct comparison with the same operational costs (e.g., fuel). The analysis can be customized for the particular cost profiles of any specific plant or hedging strategy.

Conclusion

Granular forward and options trade facilitates faster reactions when information changes, supporting more robust and live looks at the incentives to build new generation. Even if not at the hourly level, the more granular the forward trade is, the faster market incentive calculations can support new entry and the right investment in our grid. This is one reason grid operators are considering a shift from long-term annual capacity auctions to prompt seasonal auctions. Stay tuned for a discussion of these mechanics in an upcoming post.

Thanks to Peter Cramton, David Malec, and Chris Wilkens for contributing to this post.

Forward Market Design designs and builds markets that drive increased trade, investment, and information exchange. Our team has helped market participants and operators in over 100 auctions and 30 countries. Reach out to schedule a discussion on your market needs.